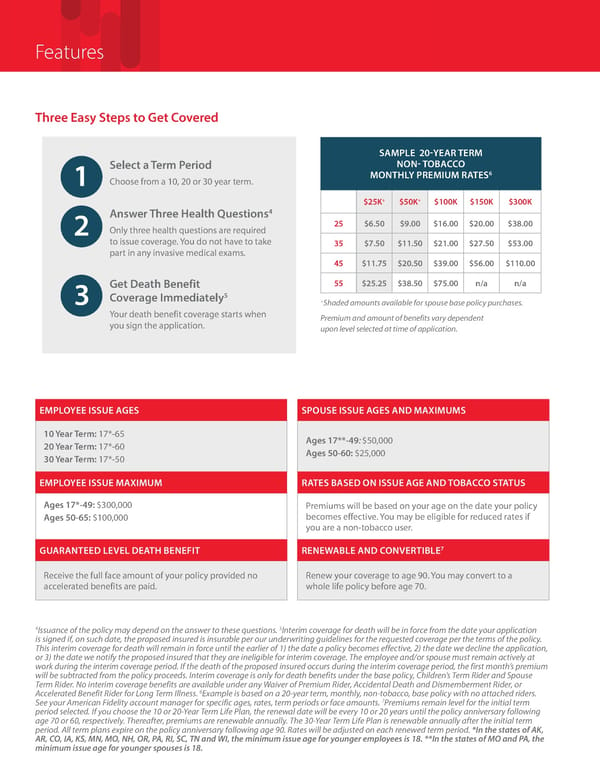

Features EMPLOYEE ISSUE AGES SPOUSE ISSUE AGES AND MAXIMUMS 10 Year Term: 17*-65 20 Year Term: 17*-60 30 Year Term: 17*-50 Ages 17**-49: $50,000 Ages 50-60: $25,000 EMPLOYEE ISSUE MAXIMUM RATES BASED ON ISSUE AGE AND TOBACCO STATUS Ages 17*-49: $300,000 Ages 50-65: $100,000 Premiums will be based on your age on the date your policy becomes effective. You may be eligible for reduced rates if you are a non-tobacco user. GUARANTEED LEVEL DEATH BENEFIT RENEWABLE AND CONVERTIBLE7 Receive the full face amount of your policy provided no accelerated benefits are paid. Renew your coverage to age 90. You may convert to a whole life policy before age 70. SAMPLE 20-YEAR TERM NON- TOBACCO MONTHLY PREMIUM RATES6 $25K+ $50K+ $100K $150K $300K 25 $6.50 $9.00 $16.00 $20.00 $38.00 35 $7.50 $11.50 $21.00 $27.50 $53.00 45 $11.75 $20.50 $39.00 $56.00 $110.00 55 $25.25 $38.50 $75.00 n/a n/a +Shaded amounts available for spouse base policy purchases. Premium and amount of benefits vary dependent upon level selected at time of application. Three Easy Steps to Get Covered Answer Three Health Questions4 Only three health questions are required to issue coverage. You do not have to take part in any invasive medical exams. 2 Select a Term Period Choose from a 10, 20 or 30 year term. 1 Get Death Benefit Coverage Immediately5 Your death benefit coverage starts when you sign the application. 3 4Issuance of the policy may depend on the answer to these questions. 5Interim coverage for death will be in force from the date your application is signed if, on such date, the proposed insured is insurable per our underwriting guidelines for the requested coverage per the terms of the policy. This interim coverage for death will remain in force until the earlier of 1) the date a policy becomes effective, 2) the date we decline the application, or 3) the date we notify the proposed insured that they are ineligible for interim coverage. The employee and/or spouse must remain actively at work during the interim coverage period. If the death of the proposed insured occurs during the interim coverage period, the first month’s premium will be subtracted from the policy proceeds. Interim coverage is only for death benefits under the base policy, Children’s Term Rider and Spouse Term Rider. No interim coverage benefits are available under any Waiver of Premium Rider, Accidental Death and Dismemberment Rider, or Accelerated Benefit Rider for Long Term Illness. 6Example is based on a 20-year term, monthly, non-tobacco, base policy with no attached riders. See your American Fidelity account manager for specific ages, rates, term periods or face amounts. 7Premiums remain level for the initial term period selected. If you choose the 10 or 20-Year Term Life Plan, the renewal date will be every 10 or 20 years until the policy anniversary following age 70 or 60, respectively. Thereafter, premiums are renewable annually. The 30-Year Term Life Plan is renewable annually after the initial term period. All term plans expire on the policy anniversary following age 90. Rates will be adjusted on each renewed term period. *In the states of AK, AR, CO, IA, KS, MN, MO, NH, OR, PA, RI, SC, TN and WI, the minimum issue age for younger employees is 18. **In the states of MO and PA, the minimum issue age for younger spouses is 18.

Term Life Page 1 Page 3

Term Life Page 1 Page 3