VEBA Plan Program Summary

This document provides a comprehensive overview of a Health Reimbursement Arrangement for public sector employees, detailing plan types, tax advantages, funding options, eligible expenses, distributions, investment options, account management, fees, and policies upon death of a participant.

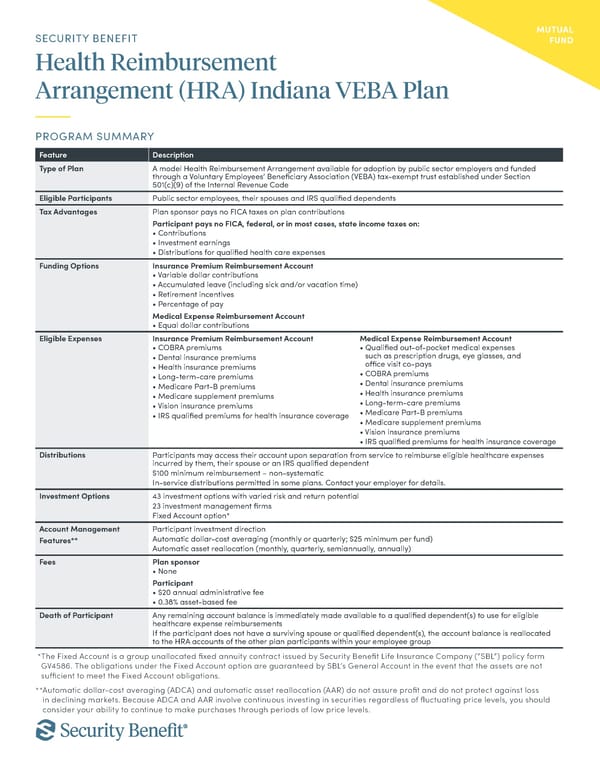

Feature Description Type of Plan A model Health Reimbursement Arrangement available for adoption by public sector employers and funded through a Voluntary Employees Beneficiary Association (VEBA) tax-exempt trust established under Section 501(c)(9) of the Internal Revenue Code Eligible Participants Public sector employees, their spouses and IRS qualified dependents Tax Advantages Plan sponsor pays no FICA taxes on plan contributions Participant pays no FICA, federal, or in most cases, state income taxes on: Contributions Investment earnings Distributions for qualified health care expenses Funding Options Insurance Premium Reimbursement Account Variable dollar contributions Accumulated leave (including sick and/or vacation time) Retirement incentives Percentage of pay Medical Expense Reimbursement Account Equal dollar contributions Eligible Expenses Insurance Premium Reimbursement Account COBRA premiums Dental insurance premiums Health insurance premiums Long-term-care premiums Medicare Part-B premiums Medicare supplement premiums Vision insurance premiums IRS qualified premiums for health insurance coverage Medical Expense Reimbursement Account Qualified out-of-pocket medical expenses such as prescription drugs, eye glasses, and office visit co-pays COBRA premiums Dental insurance premiums Health insurance premiums Long-term-care premiums Medicare Part-B premiums Medicare supplement premiums Vision insurance premiums IRS qualified premiums for health insurance coverage Distributions Participants may access their account upon separation from service to reimburse eligible healthcare expenses incurred by them, their spouse or an IRS qualified dependent $100 minimum reimbursement non-systematic In-service distributions permitted in some plans. Contact your employer for details. Investment Options 43 investment options with varied risk and return potential 23 investment management firms Fixed Account option* Account Management Features** Participant investment direction Automatic dollar-cost averaging (monthly or quarterly; $25 minimum per fund) Automatic asset reallocation (monthly, quarterly, semiannually, annually) Fees Plan sponsor None Participant $20 annual administrative fee 0.38% asset-based fee Death of Participant Any remaining account balance is immediately made available to a qualified dependent(s) to use for eligible healthcare expense reimbursements If the participant does not have a surviving spouse or qualified dependent(s), the account balance is reallocated to the HRA accounts of the other plan participants within your employee group * The Fixed Account is a group unallocated fixed annuity contract issued by Security Benefit Life Insurance Company (SBL) policy form GV4586. The obligations under the Fixed Account option are guaranteed by SBLs General Account in the event that the assets are not sufficient to meet the Fixed Account obligations. ** Automatic dollar-cost averaging (ADCA) and automatic asset reallocation (AAR) do not assure profit and do not protect against loss in declining markets. Because ADCA and AAR involve continuous investing in securities regardless of fluctuating price levels, you should consider your ability to continue to make purchases through periods of low price levels. MUTUAL FUND SECURITY BENEFIT Health Reimbursement Arrangement (HRA) Indiana VEBA Plan PROGRAM SUMMARY

VEBA Plan Program Summary Page 2

VEBA Plan Program Summary Page 2